UK Debts When Moving To Spain

Expat Tips

Published: 05 November 2014 10:58 CET

Updated: 13 October 2025 12:58 CET

Sometimes, people move abroad not just for the great weather and relaxed lifestyle, but also for the lower cost of living.

With the cost of living crisis in full swing, prices of everyday items have been rocketing, pushing more and more people into debt. Austerity measures also take their toll on all but the very affluent in society, not to mention quantitative easing, which has devalued the savings we have all worked so hard to stash away over the years.

So is it any wonder that so many UK expats look to make the break and head to Spain for a relaxed way of life, the glorious weather and just as importantly, a lower cost of living?

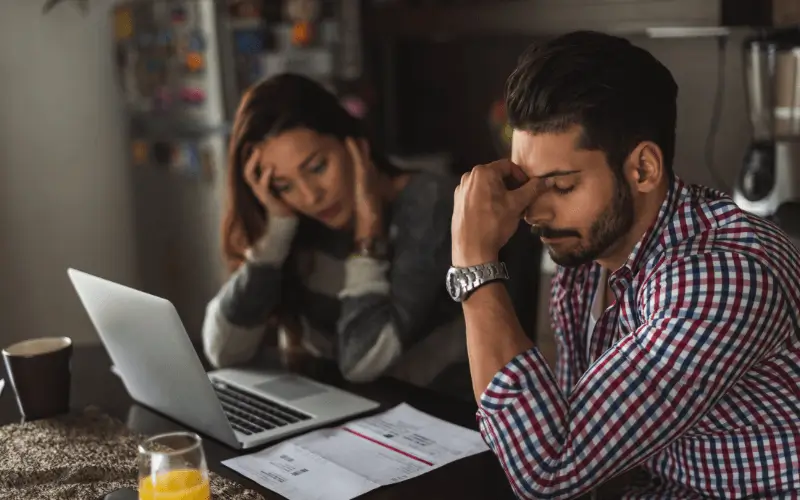

Unfortunately, many of us who leave the UK inadvertently neglect our financial commitments back home. Some even look to avoid their obligations to their creditors altogether without a thought to the potential consequences!

Having unmanageable debts with creditors and debt collectors badgering you at every moment is no fun. At one point or another, the problem will need to be dealt with.

If you do find yourself with financial 'loose ends' back in the UK, read on and learn more about the options available and your legal rights.

Please note that the following information is for guidance only. Professional, expert advice should be sought if in any doubt.

Can a Creditor or Debt Collector Find Me If I Move to Spain?

Many UK creditors have reciprocal agreements in place with similar agencies in Europe. Also, many larger businesses with a presence in both the UK and Europe may have the resources at their disposal to track you down and demand repayment of any outstanding debts.

Whether this happens or not will depend on the size of the debt and whether it is financially viable for the creditor to pursue the case.

In 2024–2025, there has been a noticeable increase in cross-border debt recovery attempts, with more UK agencies using local Spanish partners for higher-value, unresolved debts. However, routine pursuit of small debts abroad remains rare.

Digital Tracing and Banking Oversight: With expanded digital tracing (including social media checks and international bank reporting), it can be harder in 2025 to remain completely untraceable for significant debts.

If the debt is worth recovering, the creditor could seek an EEO (European Enforcement Order) which was established in October 2005. The EEO allows a creditor to enforce foreign judgements anywhere within the European Union.

Important Brexit Note: Since Brexit, the European Enforcement Order (EEO) no longer automatically applies to UK judgements for debts incurred after December 2020. However, debts from before Brexit may still be covered, and Spain and the UK maintain bilateral arrangements for enforcing certain types of debt, especially tax or court-ordered obligations.

The EEO remains the chosen method for creditors wishing to enforce domestic judgements within the EU, usually for monetary debt. For some civil and commercial proceedings, The Brussels Regulation can also be used but has a much lengthier legal process. The Brussels Regulation does not apply to criminal, bankruptcy or insolvency proceedings, or proceedings involving the status or legal capacity of natural persons, rights in property arising out of a matrimonial relationship, wills and succession.

But My Debts Are Not Very Large, Will They Bother?

In most cases, creditors will not pursue you abroad for smaller debts as it will cost them too much time and money to do so. They would also need to seek local advice and be familiar with the local laws in Spain.

So unless you owe a considerable amount, there is a very good chance that the debt will not be enforced. This does not mean that a creditor is unable to contact you either by phone or via written correspondence to get you to pay up.

This costs them very little money to do. Many creditors will do this and use threatening legal language to scare you into paying. In most cases though, they do not follow through with such threats due to the associated costs and proceedings involved in pursuing debt across international borders.

Recent Example: In 2025, several expats reported being contacted by UK creditors using Spanish-registered debt agencies for claims exceeding €5,000. These larger cases show that while small debts are often ignored, significant sums are being chased more actively.

Should I Pay My Debts Before Leaving the UK? - Your Options

There are many options when it comes to paying off your debts and it will depend on the amount owed, whether you are a property owner or employed or self-employed. These may include:

- IVA - An Individual Voluntary Arrangement is set up by an Insolvency Practitioner on your behalf with monthly payments being paid over 5 or 6 years. You will need to show a regular level of income to be accepted for an IVA. The IP will also work with you to create a repayment proposal for approval by your creditors.

- DMP - A Debt Management Plan is usually arranged via a Debt Management Company. A set amount and timetable of payments are agreed upon between the DMP Company and the creditor on your behalf in order to satisfy the debt.

- One-Off Final Settlement - In many cases, it may be possible for you to come to an agreement with your creditor for a one-off full and final settlement.

- Agreed Monthly Payment - Like the above, some creditors may be flexible and permit you to come to an alternative arrangement to pay back the debt. This could be a monthly payment over a set period. In some cases, you may have to produce a written budget and prove your level of income first.

- Administration Order - If your creditor seeks legal action and applies for a CCJ (County Court Judgement), the court may decide in favour of the creditor. If this is the case, you may be forced by the courts to repay the debt back over a certain amount of time. If the courts feel that you will be unable to repay the debt in full they may issue a 'Composition Order' in which you will have to pay back a percentage of the debt with the remainder being written off. For an Administration/Composition Order, you must owe less than £5,000.

- Bankruptcy - Bankruptcy can be voluntary or you can be made bankrupt by a creditor if you owe more than £5,000. If you decide to declare yourself bankrupt you will have to pay around £680, which comprises a £550 bankruptcy deposit and £130 adjudicator fee. Bankruptcy will usually mean your assets being seized to repay some of the debt. After one year, any outstanding debts are written off.

The 6-Year Rule - Statute Barred

Debts are not enforceable after 6 years, starting from the last payment made.

This means that regardless of any demands from creditors, they are unable to legally take any action against you in the courts once the 6 years have been reached.

Once again, this does not mean that they cannot approach you for the debt, it just means that it is no longer legally enforceable. This is commonly referred to as being "Statute Barred".

It is important to note that if the debt is acknowledged i.e. in writing (or if recorded over the phone), the clock is reset with the 6 years starting again. This does not apply if the debt is statute-barred. If the 6 years have been exceeded, the debt remains unenforceable regardless.

If you are contacted by a creditor, it is usually always best to liaise with them in writing only.

In such circumstances, having a paper trail is important.

Note that some debts are not affected by the six-year statute-barred and can be enforced after many years if required. These include tax/vat/capital gains owed to HMRC and mortgage shortfalls (12 years). If a creditor has already obtained a county court judgement, the debt can never be statute-barred. Personal injury claims also have a limitations period of only 3 years.

Spanish Tax Agency Collaboration (ANAF)

Some long-term unresolved debts, especially taxes or fines, may eventually reach the attention of the Agencia Nacional de Administración Fiscal (ANAF) through international collaboration mechanisms between Spain and the UK.

Will My UK Debts Affect My Ability to Get Credit in Spain?

No, as your credit scoring reports in the UK are not transferrable to Spain. Credit reports are also not accessible to lenders across national borders due to the different laws in each country to protect consumer data.

If a lender is based both in the UK and Spain, they could request a copy of your report internally from within the same company and use that to determine their decision.

How Will Moving to Spain Affect My Credit Score?

Firstly, if you are moving to Spain you will need to build up your credit score as you will be starting with a clean slate here.

Credit is not as readily available in Spain as it is in the UK. In most cases, you will need to build a good relationship with your bank manager. A steady job and a regular income going into your account each month will also put you in good stead when it comes to asking for any form of credit.

If at any point you wish to return to the UK to live, there is a good chance that your credit score will have been impacted negatively, especially if you have been away for several years.

In most cases, you will need to rebuild your credit score again and may find that you will need to wait for at least 3 years before you can start getting any real form of credit again.

Can I Get Help If I Live Outside of the UK?

Even if you live outside of the UK, there are still several companies and charities based in the UK that can help and advise you on your best course of action. These include:

Dealing with expat debt stress? Free financial wellbeing advice and expat support are also available through local Spanish associations in major cities.

Quick Checklist Summary:

- Always respond to creditors in writing.

- Know the 6-year rule for statute-barred debts.

- Keep detailed records of communication.

- Seek legal advice for debts over £5,000 or when facing court action.

Moving to Spain in 2025?

Since Brexit, UK citizens need a visa to live in Spain — and private health insurance that meets visa requirements is mandatory. Choose a policy with no co-payments to ensure full coverage for your Spanish visa application.

Sanitas No Co-Payment Health Insurance Plans offer complete medical cover without excess fees — perfect for UK nationals applying for non-lucrative or other long-stay visas.

Compare plans and get visa-ready cover today

Photo Credit: kenteegardin via photopin cc